The OECD released CRS XML Schema v3.0 in October 2024, alongside User Guide v4.0. For Luxembourg-based funds, ManCos, and Reporting Financial Institutions (RFIs), this is not a minor version bump — it is a comprehensive overhaul that reflects 10 years of operational experience with CRS, the rise of digital assets, and the parallel introduction of the Crypto-Asset Reporting Framework (CARF). First exchanges under the amended CRS are expected to commence in September 2027, covering 2026 calendar-year data.

At Fund-xp.lu, we help fund administrators and compliance teams in Luxembourg navigate the practical implications of AEOI regulatory changes. This article provides a structured comparison of CRS XML Schema v2.0 (published June 2019, User Guide v3.0) and the new CRS XML Schema v3.0 (published October 2024, User Guide v4.0), covering every dimension that matters for your reporting systems

Background: Why Was the Schema Updated?

The original CRS XML Schema v2.0 was designed to support the automatic exchange of financial account information between Competent Authorities and has served as the backbone of global AEOI reporting since 2019. However, it was created before the explosion of digital assets, decentralised finance, and e-money platforms — and before 10 years of practical exchange experience had revealed structural weaknesses in data quality and entity classification.

The 2023 OECD amendments to the CRS (often called “CRS 2.0”) addressed these gaps at a policy level. The XML Schema v3.0 is the technical implementation of those policy changes. The schema was approved by the OECD’s Committee on Fiscal Affairs on 23 August 2024 and published on 2 October 2024.

Critically, even financial institutions that do not manage crypto-assets are affected. The schema changes extend across all reporting scenarios, including traditional investment funds, custodians, and depository institutions operating in Luxembourg.

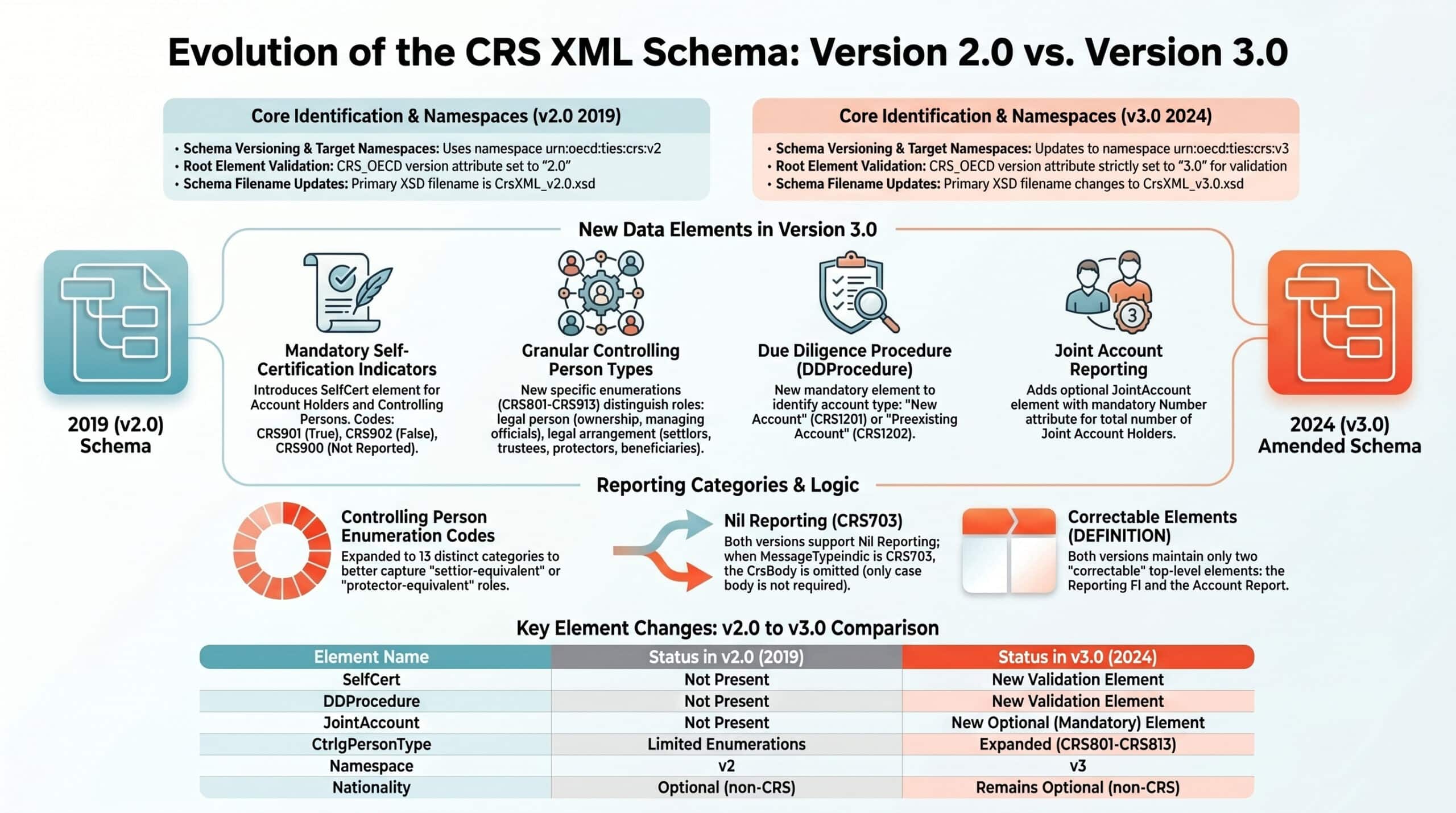

1. What does the version attribute change mean for your XML files?

The most immediate technical change is the version declaration at the root of every CRS XML file.

| Schema | Version Attribute Value |

|---|---|

| CRS XML Schema v2.0 | version="2.0" |

| CRS XML Schema v3.0 | version="3.0" |

Any file submitted with the wrong version attribute will fail validation at the receiving Competent Authority. IT teams must ensure that schema version control is embedded in their release management process and that no legacy v2.0 templates survive into 2026 reporting cycles.

2. Which new types of financial institutions are now in scope?

CRS XML Schema v2.0 was built around the classic taxonomy of Custodial Institutions, Depository Institutions, Investment Entities, and Specified Insurance Companies. Schema v3.0 extends this taxonomy to capture entities that have emerged since 2014.

New or clarified entity types in v3.0 include:

- E-money providers and payment institutions — capturing platforms that hold customer balances but were not previously classified as Depository Institutions.

- Specified Electronic Money Products (SEMPs) — a new product category covering digital wallets and prepaid instruments.

- Central Bank Digital Currency (CBDC) accounts — expressly brought into scope as CBDC pilots mature globally.

- Accounts linked to Relevant Crypto-Assets — the overlap point between CRS and CARF obligations.

For Luxembourg fund administrators, the practical implication is a review of entity classification for any clients or sub-funds operating in adjacent fintech or digital-asset spaces.

3. Do you still need to confirm self-certifications in your submission?

This is one of the most operationally significant changes in v3.0. Under v2.0, the existence of a valid self-certification was assumed implicitly — the act of reporting was taken as confirmation that due diligence had been completed. Under v3.0, a new Boolean indicator field is introduced to explicitly confirm whether a valid self-certification has been obtained for both account holders and controlling persons.

| Aspect | v2.0 Approach | v3.0 Approach |

|---|---|---|

| Self-certification confirmation | Implicit (assumed from filing) | Explicit Boolean field — must be affirmed in submission |

| Scope | Account holders | Account holders and controlling persons |

This change requires funds to verify that their onboarding and annual review workflows actually capture and store self-certification status in a machine-readable format that can be passed through to the XML submission layer. Institutions that have been storing self-certifications in PDF archives without a structured database flag will need to remediate their data infrastructure.

4. How does v3.0 distinguish between pre-existing and new accounts?

Schema v3.0 introduces a structured flag to distinguish between pre-existing accounts (those open before the jurisdiction’s CRS 2.0 implementation date) and new accounts. This distinction was previously handled in narrative guidance but not enforced at the schema level.

The new account type element also requires more granular classification of the type of account being reported (e.g., custodial, depository, cash value insurance, etc.), going beyond the high-level categorisation permitted under v2.0. Thresholds for high-value accounts and the frequency of required reviews are tied to this classification.

For Luxembourg investment funds structured as SICAVs, FCPs, or RAIFs, this means the fund administrator’s system must correctly tag each account at inception and maintain that classification through any restructuring or transfer events.

5. How should joint accounts be reported under the new schema?

Under CRS XML Schema v2.0, joint accounts were reportable but the schema offered limited structure for capturing the joint-holding relationship. Schema v3.0 introduces:

- A flag to identify whether an account is jointly held.

- A field to record the number of joint account holders.

This matters for private banking relationships and certain collective investment structures where nominee arrangements or co-investor relationships create effective joint holding. Compliance teams should audit their account taxonomy to ensure joint-holding scenarios are correctly flagged before the first v3.0 submission window.

6. What changes to entity classification and Passive NFE reporting?

Entity classification was already complex under v2.0. Schema v3.0 adds further granularity to prevent the misclassification that has been a recurring source of exchange errors and audit findings.

Key changes include:

- More detailed enumeration values for the

AccountHolderTypeand entity classification elements, reducing ambiguity at the schema validation layer. - Passive NFE reporting expansion: For Passive Non-Financial Entities, institutions must now report Ultimate Beneficial Owners (UBOs) with no exceptions, including where crypto-asset holdings are involved. This closes a loophole that existed under v2.0 where UBO reporting for certain holding structures could be argued as optional.

- Controlling person type codes have been expanded and tightened, requiring more precise identification of whether a controlling person is a settlor, trustee, protector, beneficiary, or other category.

For Luxembourg-domiciled SPVs, holding companies, and trust structures administered through local TCSPs, this represents a significant data collection uplift.

7. Which crypto-asset fields are new in CRS XML Schema v3.0?

The headline addition in CRS XML Schema v3.0 is the introduction of data elements to support the reporting of Relevant Crypto-Assets. This aligns the CRS schema with the parallel CARF XML Schema, which was published simultaneously in October 2024 and covers Crypto-Asset Service Providers specifically.

New crypto-related elements in the CRS schema include:

- Fields to capture balances denominated in crypto-assets alongside traditional fiat balances.

- Classification of accounts linked to Relevant Crypto-Assets, SEMPs, and CBDCs.

- Support for reporting exchange transactions — instances where digital assets are converted to fiat or other digital assets — which is required for complete income reporting.

The schema deliberately ensures consistency between CARF and CRS reporting to prevent arbitrage between the two frameworks. Institutions with clients holding both traditional financial products and crypto-assets must ensure that their two reporting streams — one under CRS and one potentially under CARF — produce consistent data, as tax authorities will cross-reference both.

Luxembourg funds that are not directly managing crypto-assets but whose clients hold them through third-party custodians should review whether any look-through or indicia rules bring those holdings into CRS v3.0 scope.

8. How have due diligence and indicia rules been tightened?

Schema v3.0 reflects tightened due diligence obligations at the data level:

- More frequent account reviews are required, particularly for high-value accounts. The schema supports this by requiring more detailed indicia data to be transmitted.

- Updated indicia: The v3.0 schema accommodates a broader set of residence indicators, including those relevant to digital and cross-border relationships that were not in scope under v2.0.

- Lower reporting thresholds for certain account categories, with the schema enforcing validation rules at submission that were previously only guidelines.

- Curing indicia: Where an FI has identified and resolved conflicting indicia, the schema now includes structured fields to record the outcome of that cure process, replacing the ad hoc narrative approach that was the only option under v2.0.

9. Integrated FAQ Guidance

Under v2.0, a large body of interpretive guidance had accumulated in standalone FAQ documents published by the OECD over several years. These FAQs were sometimes inconsistent with each other and required manual cross-referencing when building reporting systems.

User Guide v4.0 (accompanying schema v3.0) integrates the most relevant FAQ guidance directly into the schema documentation. This reduces ambiguity at the implementation level and means that validation rules embedded in the schema itself now reflect settled interpretive positions. Reporting institutions no longer need to maintain parallel FAQ libraries to supplement their technical schema documentation.

10.When do jurisdictions need to adopt CRS XML Schema v3.0?

| Milestone | Date |

|---|---|

| CRS XML Schema v3.0 & User Guide v4.0 published | October 2024 |

| Reporting period begins (calendar year data) | 1 January 2026 |

| First exchanges under amended CRS expected | September 2027 (for 2026 data) |

| Most jurisdictions’ local guidance | Being published during 2025–2026 |

Luxembourg’s ACD (Administration des contributions directes) is expected to publish local implementation guidance aligned with the OECD timeline. Institutions should monitor the ACD portal and ensure their AEOI reporting platforms are updated to support v3.0 well in advance of the first domestic filing deadlines.

Over 120 jurisdictions have adopted CRS to date. A coalition of 48 jurisdictions — including the UK, Canada, Brazil, Singapore, and nearly the entire European Union — committed at the G20 New Delhi Summit in September 2023 to transpose CRS 2.0 (and by extension, the v3.0 schema) into national law by 2025.

Practical Checklist for Luxembourg Funds

Based on the differences outlined above, here is a practical readiness checklist for fund administrators, ManCos, and compliance officers operating under Luxembourg CRS obligations:

- Schema version control: Ensure all XML generation systems are updated to output

version="3.0"and are validated against the v3.0 XSD before submission. - Self-certification database: Implement a structured Boolean flag in your account database for self-certification status — for both account holders and controlling persons.

- Account classification audit: Review all existing accounts to assign the new granular account type codes, including pre-existing vs new account flags.

- Joint account tagging: Identify all jointly-held accounts and add the joint-holder count field to your data model.

- Entity classification review: Audit Passive NFE and complex entity classifications to ensure UBO reporting is complete and controlling person type codes are updated.

- Crypto-asset scope check: Determine whether any of your investor base or sub-fund holdings trigger the new crypto-asset or SEMP elements — even if you are not a CARF-reporting entity.

- Due diligence workflow update: Refresh onboarding and annual review procedures to capture the new indicia fields and document curing outcomes in structured form.

- Third-party vendor engagement: Confirm with any third-party AEOI reporting providers or fund administration platforms their v3.0 implementation roadmap and target go-live date.

- Staff training: Ensure compliance, legal, and operations teams are aligned on the new definitions and classification rules before the 2026 data collection year begins.

- Test submission: Run pre-production XML validation against the v3.0 schema before the first live submission window to identify field-level errors in advance.

Conclusion

CRS XML Schema v3.0 is the most significant technical update to the Common Reporting Standard since its inception. It is not simply an extension of v2.0 — it is a structural redesign that reflects a decade of exchange experience, the integration of digital-asset transparency requirements, and a deliberate move toward machine-enforceable due diligence standards.

For Luxembourg funds and their administrators, the 2026 data collection year is already underway. The window to remediate data models, update onboarding workflows, and retrain staff is measured in months, not years. Institutions that approach this as an enterprise-wide readiness exercise — rather than a routine schema update — will be significantly better positioned when the first v3.0 exchange cycle opens in September 2027.

Fund-xp.lu provides specialist AEOI compliance support for Luxembourg investment funds, including CRS/FATCA reporting services, schema validation, and regulatory readiness assessments. Contact our team to discuss how we can support your transition to CRS XML Schema v3.0.

ACD : https://impotsdirects.public.lu/fr/echanges_electroniques/CRS_NCD.html